Fiona Clouder has wide experience of Latin America, including as the British Ambassador to Chile (2014-2018) and as Regional Ambassador, Latin America and Caribbean, COP26 (2020-2022) driving diplomatic engagement at the top of governments and business, to build partnerships and influence for the UN Climate Change Conference - COP26 – outcomes and a Net Zero world. She is also a Distinguished Fellow of RUSI (Royal United Services Institute). She previously led the FCO (Foreign & Commonwealth Office, now FCDO) strategy on Latin America (the Canning Agenda). Fiona joined the FCO in 2001, from the Research Councils (now UKRI) to build and lead the global Science and Innovation Network (UKSIN). Now working in the private sector, she continues to focus on Latin America, business links and government relations.

***************

It’s Critical: The world is in our hands – literally. It’s critical – that together we address the challenges and impacts of climate change - governments, businesses and civil society.

It’s critical that the role of mining and critical minerals for the energy transition is integrated into global policy and public awareness, it’s critical that this is done in a way that works with communities and in harmony with nature and biodiversity for a sustainable future.

It’s critical that finance is mobilised and urgent action taken. Es Tarde. It’s late – for the world and for humanity. Our world is changing, changing fast and almost beyond our grasp. With action this decade, the worst of the changes can be contained as well as bringing economic and social development. Ultimately this is about people’s livelihoods, people’s quality of life and people’s lives.

Climate Change and the Energy Transition

The IPCC (Intergovernmental Panel on Climate Change) is the United Nations (UN) body for assessing the science of climate change. IPCC reports show that the world is on a trajectory to exceed 2 o C global temperature rise, compared to pre-industrial levels, with catastrophic consequences. 1 The global temperature will stabilise when emissions reach Net Zero. To maintain global temperature rise within 1.5°C this means achieving Net Zero by c.2050.

It is still possible to meet that target. This requires emissions to peak before 2025 and to be reduced by a quarter by 2030. 50% of global emissions are now covered by climate laws and policies. There are options in all sectors to halve emissions by 2030. The technology and know-how exists. The political will has lacked momentum. But the reality continues and risks are growing, so urgent action is critical.

Much of that action relates to the energy transition - adoption of new energy sources and changes to infrastructure and energy distribution and shifts to different forms of transport, such as electric cars, as well as reduction of emissions in each sector.

Critical Minerals

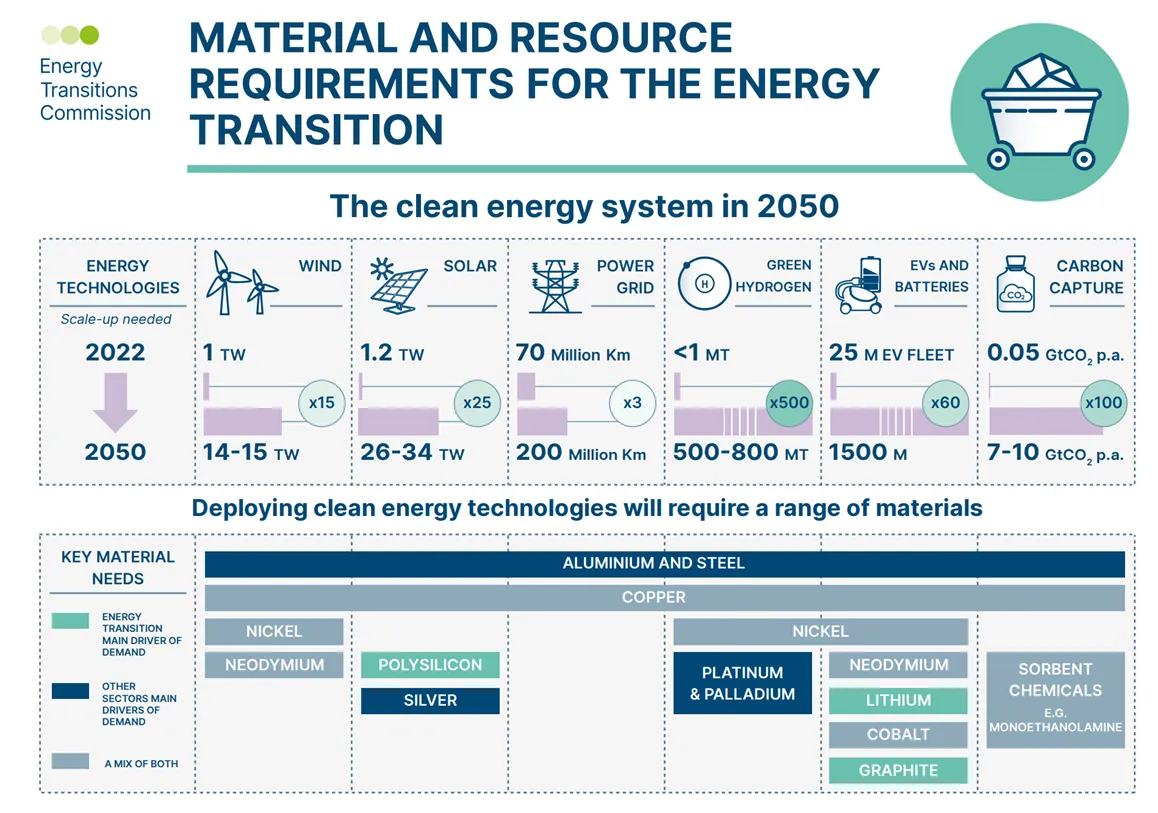

The scale and nature of the energy transition requires more mining and ‘critical minerals’. Whilst sufficient materials exist, to meet the global demand for the energy transition and to ramp up fast enough to meet requirements for 2030 poses major challenges. There is a disconnect between the aspiration and ability of countries, to meet targets for 2030 and the capacity of the mining sector to deliver. Access to and resilience of supply chains for both critical minerals and base metals is a major issue for countries across the world.

Source: Energy Transitions Commission – Material and Resource Requirements for the Energy Transition, Jul 2023

Volume and Scale-Up of Supply

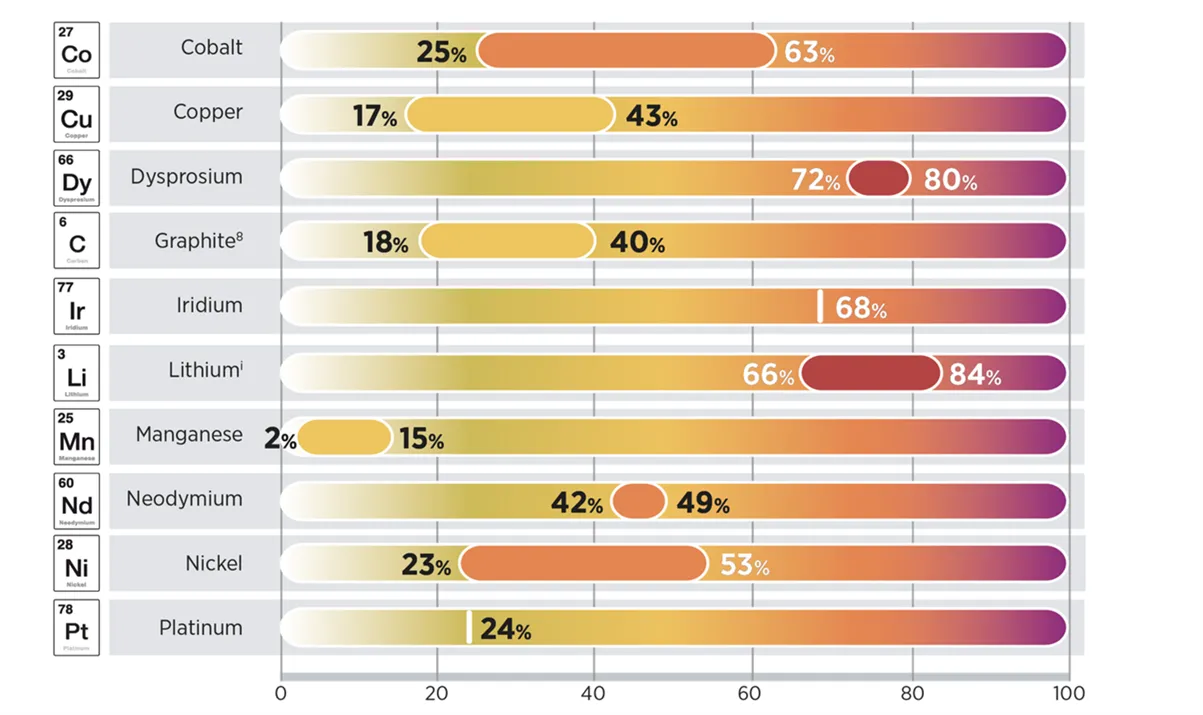

Materials are needed at scale for the new clean technologies and also for strategic technologies in space, defence and military applications. As well as new materials such as lithium, increasingly countries are realising that some core materials, such as copper and nickel, whilst abundant, will be needed – and quickly – in such volume that they too are ‘critical’. The estimated supply of some materials is insufficient to meet the anticipated demand by 2030.

Assessing disparity between current supply and anticipated demand in 2030 for selected materials

Source: IRENA (International Renewable Energy Agency): Geopolitics of the Energy Transition, 2023

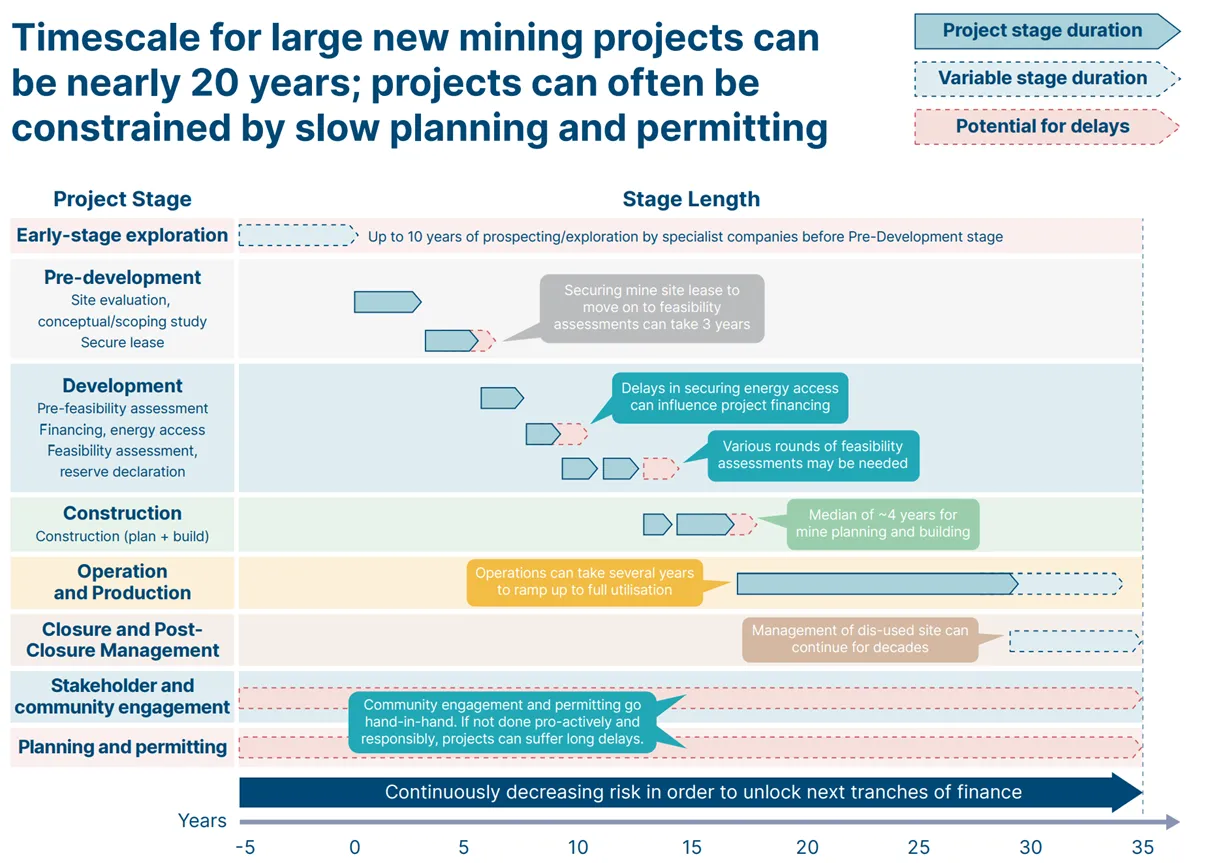

Practicalities of Supply

Mining has a long lead time from exploration and discovery to production for new sources. The rate at which an expansion of mining can take place is heavily dependent on environmental permitting and community consultation. To meet the demand for both base metals and critical minerals requires a significant increase in the number of mines. Estimates show over 300 mines are needed in the next decade to meet 2035 requirements for lithium, cobalt, nickel and graphite.

Major investment is needed at all levels. The Energy Transition Commission has identified an investment needed of between $1.1-1.7 trillion in mining, refining and recycling plants to provide adequate supply of cobalt, copper, graphite, lithium and nickel. 75% of this investment is needed in the next decade to meet the scale up required for Net Zero. 2

Source: Energy Transitions Commission – Material and Resource Requirements for the Energy Transition, Jul 2023

Responsible Supply

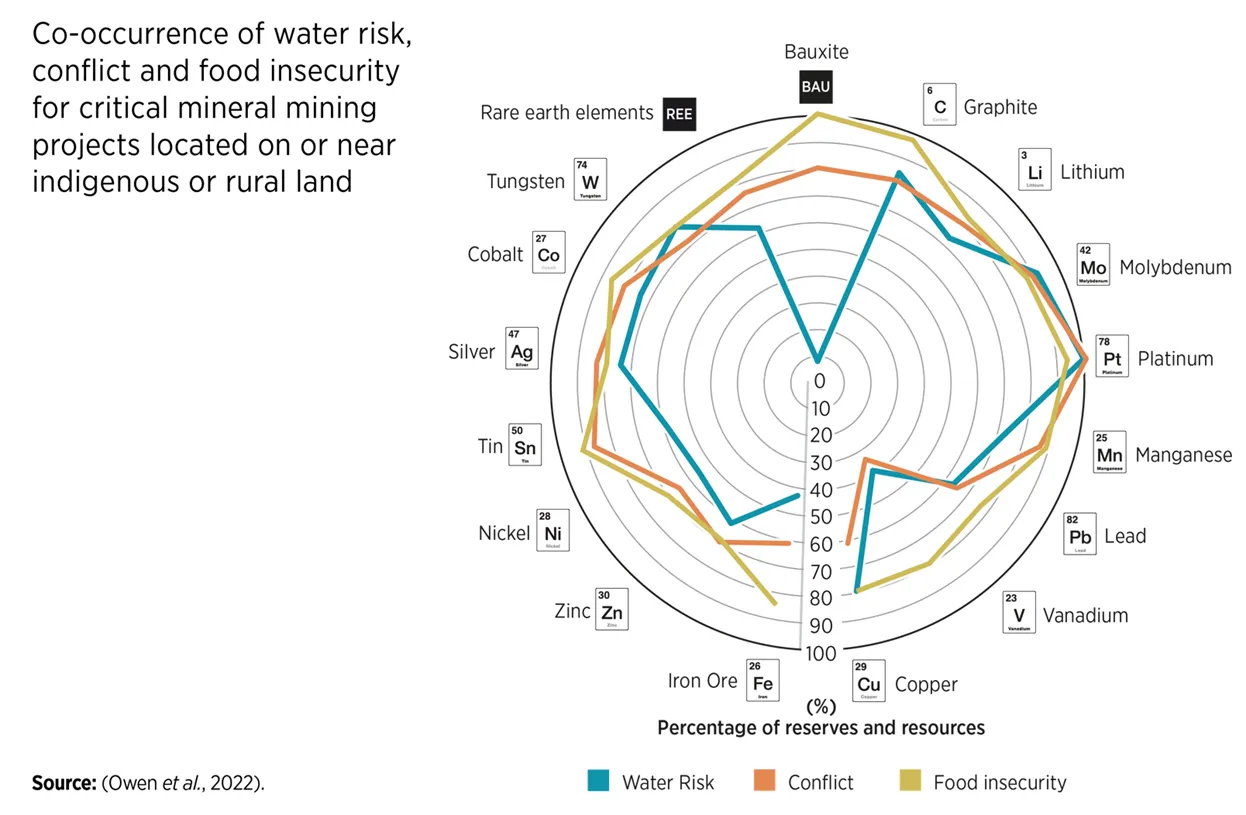

Mining and metals production account for c.10% of global greenhouse gas emissions. The industry is seeking to decarbonise, particularly focussing on downstream production and improving energy efficiency. Recycling of waste, both primary product and after secondary use, and development of a circular economy for secondary supply are increasingly important. Regulation can help with tracking and transparency of source.

Mining often takes place in water stressed areas, with competition for water exacerbating tensions with local communities. Security issues include illegal mining - particularly linked to artisanal mining, forced labour, conflict minerals, changes in land use and links to organised crime.

Source: IRENA: Geopolitics of the Energy Transition, 2023

Building trust, improving social and environmental best practice and developing public understanding are all crucial for mining to be able meet global demand. To develop the sector it is also important to attract a new generation to the labour force and develop a wider skill base for the future.

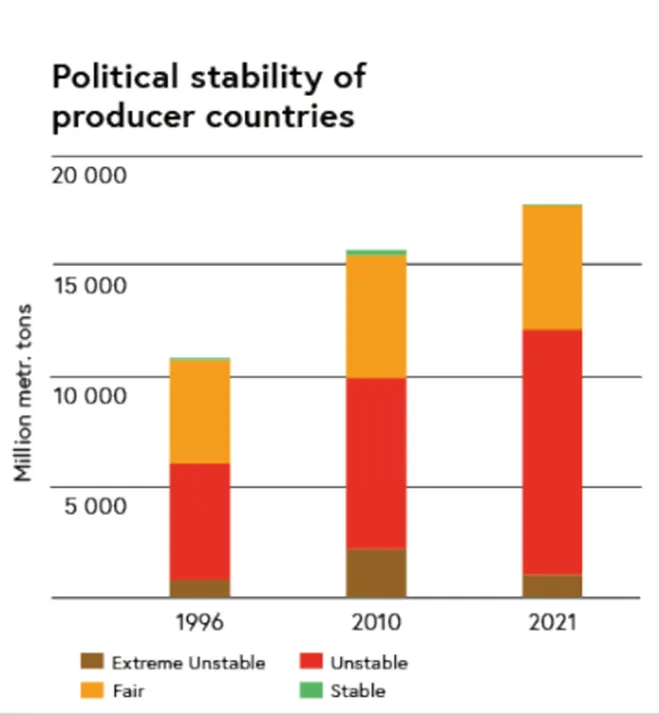

Geopolitics and Diversity of Supply

World dynamics are changing. The players with metals and mineral resources and/or processing facilities will hold a powerful position in a multipolar world that needs to achieve the transition to Net Zero. But many mine sites and critical mineral reserves are located in countries which are vulnerable to climate change, conflict and political instability, resulting in risks to critical supply chains.

Source: World Mining Data 2023 – using six dimensions of governance: (1) Voice and Accountability; (2) Political Stability and Absence of Violence; (3) Government Effectiveness; (4) Regulatory Quality; (5) Rule of Law; (6) Control of Corruption.

Global supply is dominated by a small number of countries with significant resources in certain metals and mining, with China dominating processing capability. China has also been building strategic trade relationships in Latin America and in Africa. Managing the relationship with China with regard to mining and supply chains is under discussion in the G7 and other fora.

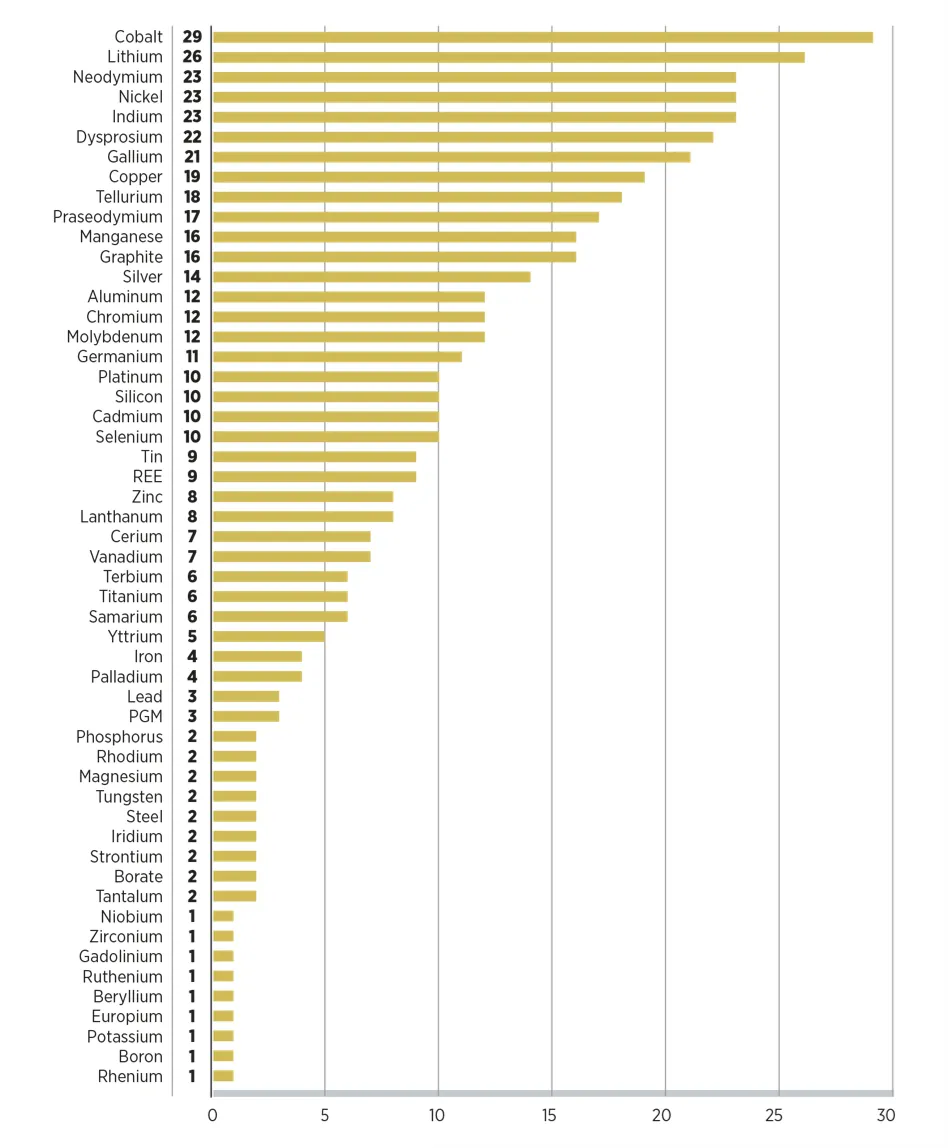

Countries are positioning for access and priority partnerships for supply. Recent initiatives include the Inflation Reduction Act, ÚSA; the Critical Raw Materials Act, European Union, the Critical Minerals Strategies published by Australia, Canada, India, Japan and the UK. The IEA Critical Minerals Policy Tracker has identified c.200 policies and regulations across the world, many of which have implications for trade and investment. 3

Energy Transition Materials Defined as Critical by Countries and Regions

(35 lists, 51 materials, 2023)

Source: IRENA: Geopolitics of the Energy Transition, 2023

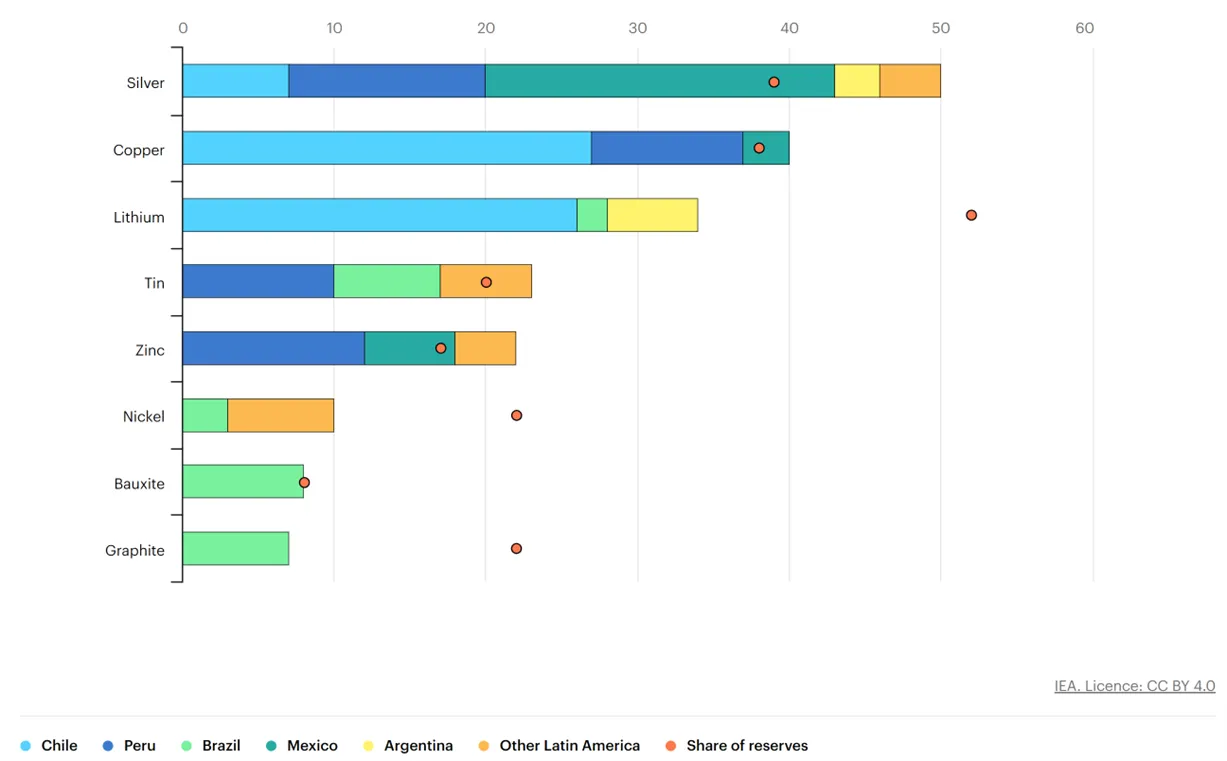

Over half of world mining production is covered by China, USA, Russia and Australia. Europe accounts for 6.8% and Latin America and Africa just over 5% each respectively 4. However Latin America and Africa hold major, in many cases unexplored, reserves of the critical minerals needed for the energy transition. Latin America has over 50% of the world’s reserves of lithium in Argentina, Bolivia and Chile; nearly 40% of the world’s copper production, principally in Chile, Mexico and Peru; and over 20% of the world’s nickel reserves, principally in Brazil.

Latin America's share in the production and reserves of selected minerals, 2021

Source: IEA - Latin America’s opportunity in critical minerals for the clean energy transition, 2023

There is tremendous opportunity for Latin America to position itself as a prime supplier to meet global demand for critical minerals, whilst also showing environmental leadership - both as a highly vulnerable region and a major holder of much of the world’s biodiversity. Regional leadership, together with the Multilateral Developments Banks, such as the IDB and CAF, and the private sector, could secure partnership agreements and drive strategic engagement to bring benefits of economic growth and social development.

Latin America, with Brazil bidding to host, is also due to hold the Presidency COP30 in 2025. There is currently a disconnect between the environmental policy world, the energy sector, the mining sector and the finance sector. Each tends to be its own echo chamber. COP30 could showcase the region and facilitate dialogue that brings together perspectives on climate, energy and mining.

As said by the IPCC – ‘Our Climate is Our Future’. To achieve the energy transition needs critical minerals. We cannot do it alone. It's critical the world gets together to address these issues, taking mining into account, in an integrated way in relation to future energy demands and environmental needs. As a new initiative, the IEA will be hosting a major international summit on critical minerals and clean energy on 28 September 2023, bringing together ministers, CEOs, investors and civil society. 5 It is a critical meeting.

2 Source: Energy Transitions Commission – Material and Resource Requirements for the Energy Transition, Jul 2023

3 IEA (2023), Critical Minerals Market Review 2023, IEA, Paris https://www.iea.org/reports/critical-minerals-market-review-2023

4 World Mining Data 2023

5 https://www.iea.org/events/iea-critical-minerals-and-clean-energy-summit

The Ambassador Partnership can help in connecting with networks around the world, with insights for business and government policy, to address global challenges